Understanding Service Awards and Taxation Benefits in the US and Canada

In the fast-paced business environment, where talent retention is a top priority, the importance of recognizing employee loyalty and longevity cannot be overstated. This is where service awards play a pivotal role in the North American businesses.

Service awards, long celebrated as milestones of employee commitment, have evolved significantly. They now serve as strategic tools that do more than just honor years of service; they play a pivotal role in shaping an organization's culture and enhancing its retention strategies.

However, navigating the complex tax laws and regulations surrounding these awards can be a daunting task. This guide aims to provide a comprehensive overview of the tax implications of service award practices in the United States and Canada, while also highlighting innovative solutions that address these challenges.

This document does not serve as an official legal or tax opinion; rather, it presents Vantage Circle's interpretation of the current tax laws about the industry of employee recognition and tenure initiatives. Its contents do not bind the IRS or CRA, and it should not be construed as a guarantee that our interpretations will align with those stated by them or the courts.

Tax Implications of Service Awards in the USA

Employee recognition holds significant value for workers, particularly millennials.

Research by SHRM reveals that when bosses acknowledge and appreciate their efforts, employees, on average, become 67 percent more engaged and are 1.3 times more inclined to remain loyal to their company.

So, apart from enhancing performance and yielding a high return on investment, employee awards also offer tax benefits. Despite being frequently overlooked, the federal income tax implications of incentive programs can result in substantial annual savings for businesses implementing reward programs.

A significant return on investment from awards is augmented by their tax deductibility. However, there are important guidelines to heed when structuring your employee awards program. As per the Internal Revenue Service, you can deduct up to $400 for non-qualified employee achievement awards and $1,600 for qualified awards given to the same employee within a year. All awards must be tangible and personal property, such as trophies or plaques.

- For an award to qualify for favorable tax treatment, it must meet two additional criteria;

- It is distributed under a written plan that doesn't favor highly compensated employees.

- The total value of all employee achievement awards given in one year must not exceed $400, excluding awards valued at less than $50.

- Cash, gift certificates, travel, vacations, event tickets, bonds, stocks, and other intangible incentives are excluded from tax-deductible awards.

- Service awards given every five years are deductible, but each year of an employee's tenure should ideally be acknowledged with an award or recognition gift.

Policies Around Service Awards in the USA

Taxation laws regarding Service Awards have changed and evolved over the years depending on industry trends and practices.

Employee Service Awards Policies:

- Award must be given in a meaningful presentation without disguising compensation.

- Not eligible for favorable tax treatment if given alongside salary adjustments or as a substitute for cash bonuses.

- Employee achievement awards are not taxable to the employee, though deductible by the employer.

Nominal Value Awards:

- Cost of awards of "nominal value" excluded from total amount of incentive awards given under established plans.

- IRS does not specify what constitutes nominal value, but most experts suggest up to $50 is nominal, while others suggest up to $100.

Exclusions from Tangible Personal Property:

- Incentive awards cannot be cash or gift certificates (unless non-negotiable for tangible personal property).

- Convertible certificates are not considered tangible personal property and do not qualify for preferential tax treatment.

- Other non-qualifying items include travel, vacations, meals, lodging, event tickets, and securities.

- Fair market value of incentive travel awards taxable to employees and deductible by employer as compensation.

Length of Service Awards Exclusions:

- Excluded from employee income if received after first five years of service with the awarding employer.

- Exclusion applies if an employee hasn't received another length of service award from the employer for at least five years.

Tax Implications of Service Awards in Canada

Non-taxable Conditions

-

Under the updated CRA's administrative policy, if you provide your employee with a service award, the benefit is not taxable if all of the following apply;

-

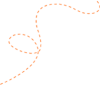

It is a non-cash gift or award, including gift cards that meet all conditions for the card to be considered non-cash.

-

It has been at least 5 years since the last time the employer gave the employee a long-term service award

-

The Fair Market Value (FMV) of the award is $500 or less (including taxes).

Taxable Award Conditions

- If the service awards you provide to your employees do not meet all the conditions above, it is a taxable benefit.

- Service awards have their own $500 limit. The unused portion of the $500 limit for long-service awards cannot be applied to non-cash gifts and awards.

Understanding Tax Regulations

United States

The Internal Revenue Service (IRS) has established specific guidelines for the taxation of service awards, which vary based on the type of award and the duration of the employee's service. Here are the key points to consider:

-

Cash Awards: Cash awards, such as bonuses or lump-sum payments, are generally considered taxable wages and are subject to federal income tax withholding (FITW), Social Security and Medicare taxes (FICA), and unemployment taxes (FUTA), as well as applicable state and local payroll taxes.

-

Non-Cash Awards: The tax treatment of non-cash awards, such as gift cards, merchandise, or experiences, depends on their nature and value. While infrequent gifts like fruit baskets, wine, or event tickets are generally non-taxable, gift certificates or cash equivalents are considered taxable income.

-

Length of Service Awards: Length of service awards are excluded from employee income if received after the first five years of service with the awarding employer and if the employee hasn't received another length of service award from the same employer for at least five years.

Canada

The Canada Revenue Agency (CRA) has similar guidelines for the taxation of service awards, with some variations:

-

Cash Awards: Cash awards are generally considered taxable income and subject to income tax withholding, Canada Pension Plan (CPP) contributions, and Employment Insurance (EI) premiums.

-

Non-Cash Awards: Non-cash awards, such as merchandise or gift certificates, are considered a taxable benefit for the employee and must be included in their income for the year.

-

Length of Service Awards: Length of service awards are generally non-taxable if they are awarded for long-term service (typically five years or more) and are not cash or cash equivalents.

Addressing Tax Compliance with Innovative Solutions

To ensure compliance with these complex tax regulations and streamline the administration of service award programs, organizations are increasingly turning to innovative solutions offered by external platforms and service providers.

One such solution is Vantage Circle's Service Awards Platform, which offers a range of features to simplify the process while ensuring compliance with tax laws in both the United States and Canada. The following are ways through which Vantage Circle's features can ensure this:

Non-Cash Rewards

Gift Cards

-

De Minimis Fringe Benefits: According to the IRS, some low-value benefits provided to employees on an infrequent basis can be treated under de minimis fringe benefits and would not be termed as taxable. Sometimes gift cards with a small denomination fall into that category.

-

Achievement Awards: Gift cards under qualified plan award for the length of service is excludable from an employee's tax unless they exceed a certain limit.

Merchandise and Experiences

- Incentive Programs: Merchandise and experience awards can be designed as part of incentive programs, which, under certain conditions, could be eligible for better tax treatment.

Vantage Benefits

Corporate Discounts

- Employee Discounts-Free from Taxes: The Internal Revenue Service, in this case, doesn't have a requirement for the payment of tax on employee discounts on services and merchandise, so long as it passes their articulated criteria of not exceeding the gross profit percentage on goods or 20% on services.

Cashback Offers

- Non-taxable Cashbacks: The cashback rewards coming out of any employee discount program would, at many times, be structured expressly such that the cashback would not be considered as a top-up proportion – hence, no extra tax to be bear.

Service Awards

Length of Service Awards

- Qualified Plan Awards: This would represent non-cash service awards for length of service; for instance, a service yearbook or long service award would be tax-free up to $1,600 for the qualified plan award if certain conditions are met, such as the actual award being given as part of some sort of meaningful ceremony.

For tax purposes, the awards need to have records up to date and under what conditions the awards are given. Also, it is important to have IRS guidelines up to date since they may change.

Sources

-

[IRS Publication 15-B] : Employer's Tax Guide to Fringe Benefits.

-

[IRS Fringe Benefit Guide]: A candidate description of diverse fringe benefits and their taxability.

-

<[IRS Fringe Benefit Guide]: Detailed guidelines on gift card taxation, on how to include them as taxable income.

Leveraging these aspects, Vantage Circle can be the most effective way for organizations to deliver important rewards and benefits to powerful employees, keeping their tax liabilities optimal in the US.

Tax Restrictions

-

Limitations for Non-cash Awards: According to the IRS, certain non-cash awards given to employees as part of length-of-service award programs are exempt from taxable income, subject to certain limitations. Companies can keep employees below the threshold for tax-free status by offering a range of clever, non-cash, personalized award options.

-

Tangible personal property: Awards of tangible personal property, for example, luxury items that meet the requirements of the Internal Revenue Service criteria for length-of-service awards, are eligible for exclusion from an employee's gross income. This allows organizations to reward employees without adding to their tax liability.

Conclusion

As organizations in North America strive to attract and retain top talent, effective service award programs have become a strategic imperative. However, navigating the complex tax regulations surrounding these programs can be a significant challenge.

By leveraging innovative solutions like Vantage Circle's Service Awards Platform, organizations can not only ensure compliance with tax laws but also create a more engaging and meaningful recognition experience for their employees, ultimately driving increased loyalty, engagement, and retention.

This article is written by Vaishali Goswami, a member of the content team at Vantage Circle. Between being an active writer and a traveler, Vaishali can be found in books about psychology and human behavior. For any related queries, contact editor@vantagecircle.com.